Below is a brief introduction to 1031 exchanges. Here you will gain knowledge about key benefits, basic rules and guidelines for successful implementation using a Delaware Statutory Trust.

In most circumstances, the use of a qualified intermediary is required to successfully complete an IRC Section 1031 tax-deferred exchange. Treasury Regulation refers to the entity that facilitates a 1031 exchange as a qualified intermediary. A qualified intermediary is sometimes referred to as an accommodator, facilitator, intermediary or QI, which it defines as follows:

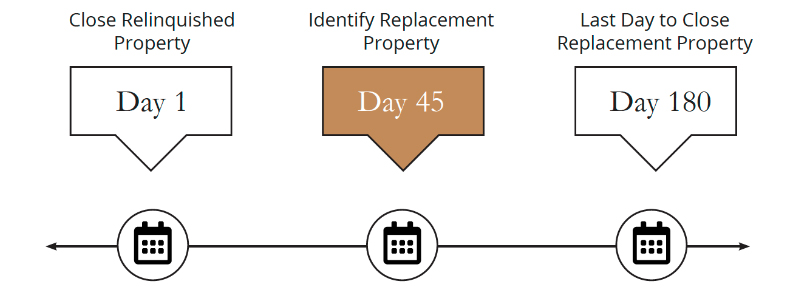

The time requirements in a 1031 exchange are very specific. From the close of escrow on the sale of the relinquished property, a taxpayer must properly identify potential replacement properties within 45 calendar days and close on the replacement properties within 180 calendar days.

For exchange purposes a like-kind replacement property means any property held for investment or business use. For Instance – A rental home could be exchanged for:

A DST is like-kind. Revenue Ruling 2004-86 (July 20, 2004) explains how a DST described in the ruling will be classified for federal tax purposes and whether a taxpayer may acquire an interest in the DST without recognition of gain or loss under section 1031 of the Code.

The common objective in a 1031 exchange is disposing of a property containing significant realized gain and acquiring a like-kind replacement property so there is no or little recognized gain. In order to defer all capital gain taxes, a taxpayer must balance the exchange by following these guidelines.

DST's secure non-recourse financing backed by the real estate within the trust. The average DST loans range between 45% and 65% loan-to-value. When an investor purchases an interest in a DST, the investor will inherit or be assigned a portion of the loan.