A Delaware Statutory Trust (DST) permits fractional ownership where multiple investors can share ownership in a single property or a portfolio of properties. The DST qualifies as replacement property for an investor's 1031 exchange. A DST takes all operational decision-making and active management activities out of the hands of the investor and places it into the hands of an experienced sponsor-affiliated trustee.

Section 1031 of the Internal Revenue Code provides an effective strategy for deferring capital gains tax that may arise from the sale of a business or investment real property. By exchanging the real property for like-kind real estate, real property owners may defer taxes and use the proceeds to purchase replacement property. Like-kind real estate includes business and investment real property, but not the property owner's primary residence.

It is important to note that several specific requirements must be met in order to successfully execute a 1031 exchange transaction. Most importantly, the total purchase value of the replacement property must be equal to or greater than the value of the relinquished property sold. Additionally, all the cash proceeds must be used, and the debt can be replaced with new debt or additional cash. In other words, additional cash can make up for a shortfall in debt placed on a replacement property, but additional debt cannot make up for a shortfall in cash invested in a replacement property. Any "unreplaced" debt or equity would be considered boot and would likely have tax consequences. Prospective investors should consult their tax advisors regarding a 1031 exchange and their specific situation.

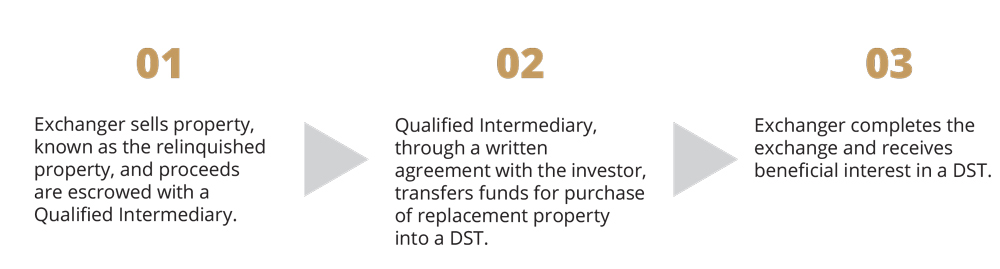

A 1031 exchange involving an investment into a DST typically has three steps

The QI is a company that facilitates Section 1031 tax-deferred exchanges. The QI enters into a written agreement with the investor where the QI transfers the relinquished property to the buyer, while transferring the replacement property to the investor pursuant to the exchange agreement. The QI holds the proceeds from the sale of the relinquished property in a trust or escrow account in order to ensure the investor never has actual or constructive receipt of the sale proceeds, which would trigger capital gain consequences.

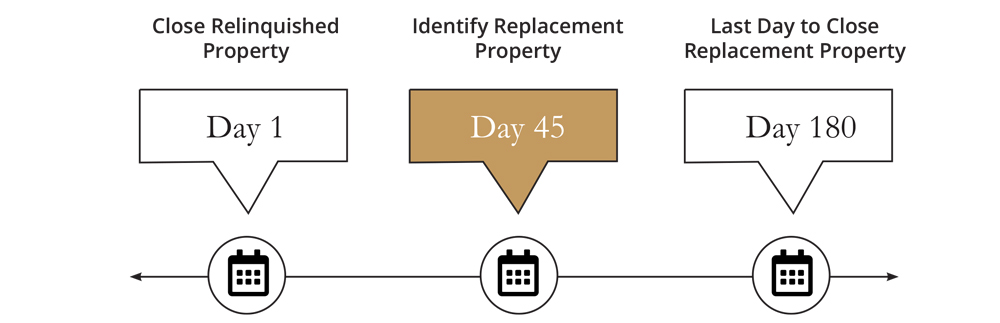

The time requirements in a 1031 exchange are very specific. From the close of escrow on the sale of the relinquished property, a taxpayer must properly identify potential replacement properties within 45 calendar days and close on the replacement properties within 180 calendar days.

To complete a successful Section 1031 tax-deferred exchange, the replacement property must be like-kind to the relinquished property. Some examples of like-kind properties include:

Any real estate held for productive use in a trade or business or for investment purposes is considered like-kind. A primary residence would not fall into this category, however, vacation homes or rental properties may qualify in some situations.

Full Replacement of Relinquished Asset in a Timely Manner

DSTs are a popular solution that can be used to address the changing nature of investment property owner's objectives as they age. A DST investment can be selected and identified before the close of the relinquished asset, simplifying the 1031 exchange process.

BootAny leftover equity or debt in a 1031 exchange is subject to taxable gain. A DST can solve the tax problem for cash boot or mortgage boot.

Back up - The Pitfalls of Day 45Don't get sidelined by Day 45. A DST has little close risk as the trust has secured title, and the financing terms are set and closed. A DST can be a backup to a first choice on Day 45 of the identification process.

Estate Plan (Swap Until You Drop)Streamline the transfer of real estate wealth with fractional ownership of a DST. Your heirs will receive ownership upon death at a step-up in basis.

No Management Responsibilities

The DST is the single owner and agile decision maker on behalf of investors.

Access to Institutional-Quality PropertyMost real estate investors can't afford to own multi-million dollar properties. DSTs allow investors to acquire partial ownership in properties that otherwise would be out-of-reach.

Limited Personal LiabilityLoans are non-recourse to the investor. The DST is the sole borrower.

Lower Minimum InvestmentsDSTs can accommodate much lower minimum investments, whereas 1031 exchange minimums often are $100,000.

DiversificationInvestors can divide their investment among multiple DSTs, which may provide for a more diversified real estate portfolio across geography and property types.

At its core, the DST is a real estate asset. The inherent risks associated with any real estate investment should be considered before investing and compared against the available benefits. For example, one should consider property values and operational performance, or the ability to generate cash flow, and the impact by changing economic, demographic and climatic conditions. In addition, elements of the DST's structure and requirements should also be understood and considered in conjunction with an investor's objectives.

Sponsors are Important:

The DST sponsor is the entity that creates the DST to hold and manage real property and arrange for issuing beneficial interest to investors. The sponsor locates and acquires the real estate through comprehensive due diligence and secures financing for the trust. Who the sponsor is, their track record, and long term experience can often be one of the most important decisions when selecting the DST.

No Liquidity and Potential Losses:The purchase of any DST sponsored program is speculative. It is suitable only for persons who can accept the lack of liquidity and willing to put their entire equity investment at risk. The sponsor company spends a significant amount of time and resources on due diligence, underwriting and analysis when acquiring the properties. However, there is still no guarantee that an investor's objectives will be achieved. As an investor, taking the time to review the offering documents and understanding the real estate is an integral part of the process.

As a Passive Investment, the Sponsor Maintains Control:With a DST, investors can still enjoy the benefits of owning real estate without dealing with day-to-day landlord activities. The investor is now relying on the sponsor, a professional real estate investment management firm, for all property operations and decisions and does not have any voting rights. Being willing to give up control and decision making is an important part of the DST.

The Imbedded Fees:With any investment, there is always a cost. A DST has three major phases: acquisition, operations and disposition. Each phase will incur its economic costs associated with the investment. Costs include management fees, disposition fees and some upfront fees, referred to as "Load." Upfront fees are all capitalized into the DST/investor transaction, and can consist of commissions, broker-dealer allowances, offerings, organizational costs and financing fees. Engaging with a trusted professional to understand each invested dollar's application in a DST is very important to understand.

Specific risk factors are detailed in the Private Placement Memorandum of each DST and should be reviewed and evaluated.