From time to time, various investors or their professional tax or legal advisors have a negative impression of passive fractional ownership investment programs generally structured as TICs or DSTs. In most cases these impressions are due to either a previous negative experience with a program or a potential lack of understanding of risks or mitigation strategies.

Understandably, the most common concerns are lack of control and fees (load). Both are valid concerns. For the investor who wants or needs control, or would rather spend their time and effort sourcing, contracting, structuring, doing due diligence, and operating the asset, the DST is not a suitable choice.

Control

There are many benefits to investing in a DST such as diversification, asset quality, regular distributions, and no management responsibilities. With a DST, investors can still enjoy the benefits of owning real estate without dealing with the day-to-day landlord activities. Although this may be a plus for some, others do not want to give up their management responsibilities. With a DST, investors do not have operational control, nor can they make management decisions. As an investor you are relying on the program sponsor (an experienced, long-term institutional real estate investment management firm).

An investor needs to weigh the positives and negatives based on their individual situation to decide if it is the right investment. Alternatively, for the investor needing control and wanting to actively manage the investment, they are generally trading control for diversification and asset quality.

Fees

With any investment, there is always a cost. A DST has three major phases, acquisition, operations, and disposition. Each phase will incur its own economics. As real estate investors' operational costs and disposition fees are not out of the ordinary. You may, however, find some upfront fees, referred to as "load," that need explanation. The load in a DST will include commissions, Broker-Dealer allowances, offering and organization costs, financing fees, etc. and these are all capitalized into the DST/Investor transaction (Full Offering Purchase Price). Across the industry these fees are typically in the range 7-10% of equity. When comparing these fees to the associated costs of a direct purchase by the investor, we find that the DST fees would only be marginally higher to the direct purchase if the Due Diligence is comparable, and that differential is mainly associated with the DST structure and regulations. We view the premium as a trade off to the ease of use for the investor.

Other Risks

Of course, there are many other risks to be carefully considered, such as lack of liquidity, economic volatility, and environmental and market risk. Many of these would be directly comparable to a direct purchase.

Assuming the investor can satisfy themselves with these considerations, the DST may be an appropriate solution. The investor can further mitigate their risks with an appropriate diversification strategy and managing their concentration in illiquid investments. And for exchange investors, balancing the potential risks against the potential tax liability can support the decision.

In the end, the investor's total return is usually the ultimate measure of success. We would argue that the average returns, especially in certain asset classes, are comparable and sometimes better than the alternative options (e.g., a DST vs a NNN-leased investment or others). To further improve the potential success, working with an experienced advisor with both market knowledge and sponsor company knowledge can support the selection process.

As with any industry, certain companies have better track records than others. By design, we work most closely with firms with which we have long-term experience and those with good track records. We have found that many people who have had a negative experience or impression have typically worked with perhaps less experienced or smaller sponsors, or they did not properly understand the risks going before making the investment.

Please see the Full Cycle Track Records for 3 of the major sponsors we work with. Please look for the Multifamily asset class individual and average returns, as this class has historically been a strong performer.

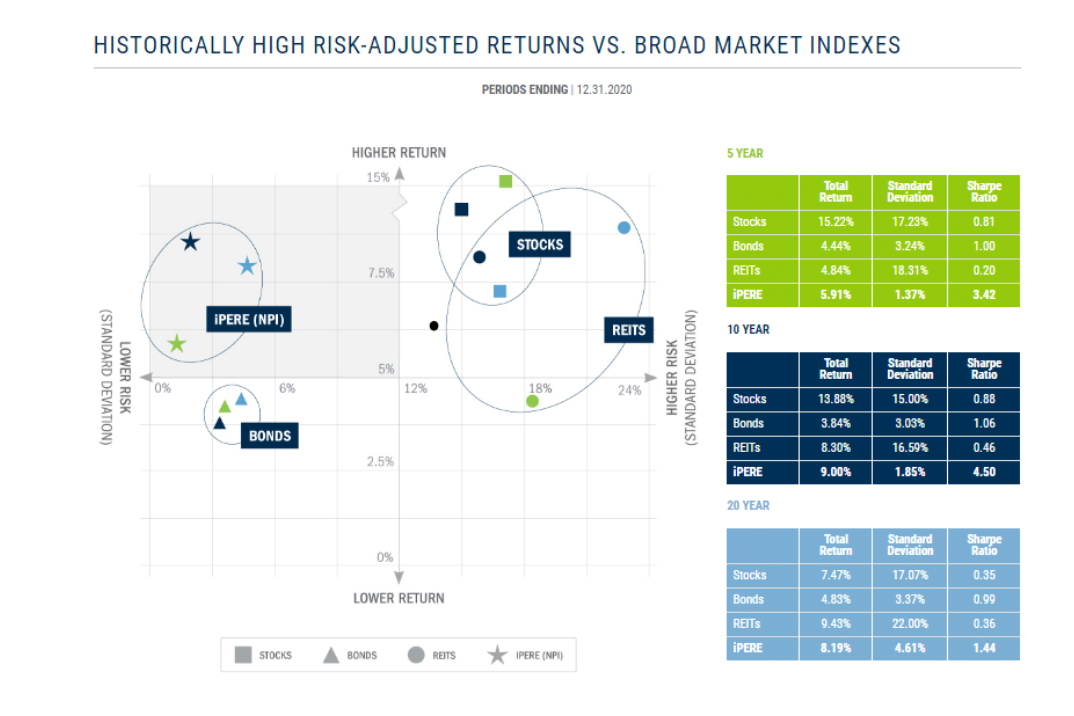

As an aside, the chart below makes a strong case for Institutional Private Equity Real Estate (iPERE) like the DST compared to other asset classes